Financial Inclusion in Russia by National Agency for Financial Studies - HTML preview

Download the book in PDF, ePub, Kindle for a complete version.

EXECUTIVE SUMMARY

The G20 Financial Inclusion Indicators suggest that financial inclusion should be measured in three dimensions: ( i) access to financial services, ( ii) usage of financial services, and ( iii) quality of products and service delivery. To form a comprehensive view, the G20 Financial Inclusion Indicators include both supply-side and demand-side data. In addition, they provide further insight into access and usage aspects by including indicators on emerging branchless delivery channels such as mobile banking.

In 2012, CGAP conducted a Financial Inclusion Landscaping study in Russia that highlighted the need for comprehensive and detailed data on the picture of financial inclusion — and exclusion — in Russia, to better understand specific profiles and needs of the unbanked and underbanked, as well as barriers preventing people from accessing and using financial services. The goal of this research, conducted by the National Agency for Financial Studies (NAFI) with support from CGAP and Beyond Philanthropy during April–June 2014, was to fill in some of the information gaps with respect to the demand-side aspects of financial inclusion in Russia. The key findings and conclusions of the research, organized around the three dimensions of the G20 Financial Inclusion Indicators, are presented below.

Access to financial services

- Physical access to financial services in Russia remains a challenge; remote and rural areas are insufficiently covered with financial service provider branch networks, POS terminals, and communications infrastructure. Relatively high aggregate statistics on physical access appear to hide the issue of insufficient infrastructure, as they do not capture the supply of physical access points in low-population areas.

- This is confirmed by data on customer satisfaction with physical access infrastructure: there are significant variations in satisfaction levels by region, as well as by settlement type (i.e., city/town/village). For example, in rural areas, satisfaction levels are 11 percent lower than on average, and in regional capitals they are 5–15 percent higher than average. The smaller the settlement, the more often respondents express the need to increase the number of service points.

- From the demand-side perspective generally, physical access seems to be of relatively lower importance compared to the factors related to provider reliability, and especially the high complexity of financial products and services available.

- Recognizing the physical access issue, financial service providers mention the high costs of physical infrastructure development, but more in terms of excessive regulatory requirements, which increase the costs and adversely affect providers’ business case.

Usage of financial services

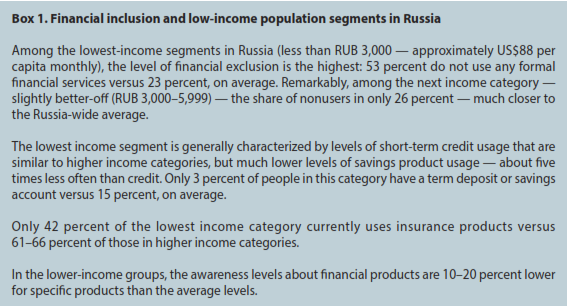

- The overall usage of financial services in Russia has not changed since 2011: 23 percent of respondents report not using any of formal financial services. For all types of financial products, the level of usage strongly and directly correlates with income levels. There is a remarkable difference in financial service usage among the lowest income segment: 53 percent of respondents in this category are not using any formal financial services — more than double the Russia-wide average figure.

- A trend to watch both for providers and policy makers is much higher usage of credit than savings products (39 versus 24 percent; the latter even lower when only term savings products are considered — 15 percent). This trend is especially pronounced among the lowest income segments, where the usage of savings products is five times lower than of credit products; the usage of credit is approximately the same as in the other income categories. On the one hand, among the dangers of an excessive credit usage is customer over-indebtedness; on the other hand, through responsible promotion of both credit and savings services and their increased usage, providers can advance financial inclusion, as they can influence both borrowing and savings behaviors. The challenge is how providers can be better attuned and more responsive to the needs of this segment through the development and marketing of products that offer good value propositions for customers and that are, at the same time, profitable and sustainable for providers.

- Higher awareness levels about financial products and services do not necessarily bring about higher usage: while the aggregate figures on the usage of financial products highly correlate with awareness levels, disaggregated statistics often show either no or even inverse correlations between the awareness and usage for specific segments.

- Personality types identified during this research based on prevailing attitudes about money do not correlate strongly with the usage of specific financial products, but they are slightly better predictors of the choice of financial service delivery channels (although further research may be needed in this area as this research was a first attempt to establish such correlations). Overall, sociodemographic characteristics tend to be stronger predictors for both the types of products customers use and the channels they choose to obtain these products and services.

- Financial products used the most are those that are provided to customers by third parties (e.g., employers and government) rather than those actively sought by the customers. The issuance of these provided products does not result in a more active usage of other financial services. This presents both a challenge as programs such as those aimed at universal bank account coverage may not result in higher financial service usage generally; but at the same time, it is an opportunity for providers to develop various products that account for this type of customer financial behavior.

- Insurance products are the least used among financial products, which suggests a high potential for their development — provided that products are better understood by customers and, possibly, are better suited for their needs.

- The potential of innovative delivery channels for expanding the range of financial services will largely depend on customer perception of these channels as more reliable and more easy-to-understand and use than traditional channels. Currently, traditional channels such as bank branches are mostly viewed as the most reliable, though the least convenient, by a majority of Russians.

Quality of financial services

- The research substantiates the need to increase levels of financial literacy. Qualitative research of financial literacy-related issues confirmed the available quantitative survey evidence on relatively low levels of financial literacy: many customers do not distinguish between products or are not even aware that they are using some of them. The findings reinforced other results of this research signaling that customers have a strong need for simpler, easier-to-understand financial products and services presented in a more standardized way.

- Among the most important factors affecting the choice of financial service provider and decision to use financial services is high complexity of financial products for customers and lack of standardized presentation of terms and conditions of financial products. There is room for providers to be more proactive in making their products more easy-to-understand for customers.

- Policy makers may want to consider introducing standardized financial product description and disclosure formats. They may also consider regulating the terminology that providers can or cannot use — especially with respect to savings products, to clearly denote which of them are covered by the deposit protection scheme. Such measure could be complemented by financial literacy campaigns explaining the descriptions, disclosure formats, and terminology to customers.

- Finally, overcoming common stereotypes with respect to financial service providers and products (such as negative attitude to credit or a belief that savings make sense only for large amounts of money) will be necessary to increase financial inclusion in Russia. This could be a task for both policy makers and providers of financial services.