Cash Flow Management Handbook by Mwesige Emmanuel - HTML preview

Download the book in PDF, ePub, Kindle for a complete version.

BEST PRACTICES OF CASH FLOW MANAGEMENT

CASH FLOW STRATEGY

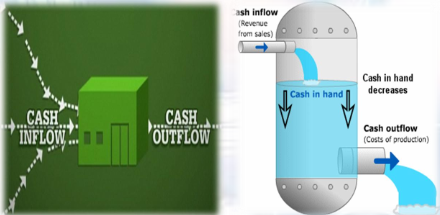

Cash is the lifeblood of your business. If you have a good business model and you’re great at managing cash, your company will be wildly successful. But if you’re not skilled at managing cash then even if you have a good business model, you will likely wind up being a statistic.

Many small to medium size business owners focus on profits. However, that’s not enough to truly be successful. Your profit is just the amount that your income exceeds the expenses you incurred to earn that revenue.

You also need to understand your cash flow: the net amount of money flowing in and out of your business. Your cash flow should cover the cost of your operations-including payroll and other expenses, including paying yourself and investing in future growth.

There are three main sources of cash. You can get cash from operating activities, investing activities, and financing activities. If you want to understand your cash flow, you need to keep great records of the cash coming in and going out of your business.

MANAGING CASH FLOW

For many business owners, one big obstacle to business success is how they think about money. When it comes to cash, ask yourself, do you start from a position of scarcity and fear or one of abundance?

Why is this so important? Well, if you operate from a position of fear, you will tend to avoid dealing with critical financial issues until you absolutely have to. Most successful CEOs deal with money issues up front, early, and often. They are upfront with clients and suppliers about what it takes to separate money from their wallets-before doing any work. That mindset is critical to being great at managing cash flow.

You also need to know whether you’re a “big spender” or frugal. A big spender can’t keep money in the bank. When cash comes in, you’re going to spend it. A big spender can implement all cash flow management techniques but, you won’t overcome your cash flow problems if money always goes out faster than it’s coming in. If you stop to think about how much gross revenue you need to get the cash to buy something-it will make you think twice.

UNDERSTANDING CASH FLOW

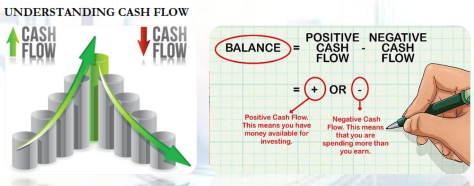

Let us begin by understanding the difference between profits and cash. Profits are what show up on the bottom line of your income statement. That shows whether you sold services or products for more than it cost to deliver them.

Cash flow focuses on the timing of when your company gets paid and when it has to pay someone else. Your operating cash flow is the cash generated by your company’s normal operations. A really successful business will have positive operating cash flow that is greater than its profits.

Your free cash flow represents the amount of cash your business generates minus any capital expenditures. You use free cash flow to repay debt, reinvest in your company, or pay out distributions to the owners. The goal of your business is to generate free cash flow because it creates wealth for you-the owner-and generates money so you can grow your business.

Your cash flow-the timing of when cash comes in and goes out of your company-is usually on a different timing than your earned income or paid expenses.

It’s important to understand: Your business can be making a profit but still have a negative cash flow. Why? Because regardless of the amount of profit you made, if the amount of cash you received is less than or equal to what you spend, then you’re eating into your cash reserves. In the long run, it negatively impacts your ability to pay your bills, which in turn impacts your ability to operate

The reasons for a negative cash flow can always be found in your sources and uses of cash report. For example, the sources and uses of cash report will show if you have an increase in receivables because you made sales “on account” but didn’t receive cash. Or you might have used cash to pay down some debts, like paying off your credit card balance.

On the flip side, you might receive cash from upfront deposit payments from your clients and get paid before you have incurred expenses. We’ll show you how to use your clients as a funding source instead of them using you as one, (which is what happens when you provide services first and bill clients later).

Some business owners believe they can sell their way out of cash flow problems. When they try to, they often make poor operational decisions like taking on low-profit, demanding, or even “bad” clients just to get money in the door.

There are several big bucket ways to improve your cash flow. In this guide, we’ll show how to optimize your collection and pricing strategies, manage your expenses and make smart hiring and firing decisions.

We will show the impact of accepting only “good money” clients, and how you can adopt smart and timely billing policies that minimize the amount of time between providing services and receiving payment. By making better, more strategic decisions about how you run your business, you can begin to improve your cash flow

How do you keep from getting into a cash flow crunch so deep that you worry about making payroll? The answer is to have effective pricing, billing methods, sales policies, collections processes, and expense management that all improve your cash flow.

SOME OF THE BEST PRACTICES IN CASH FLOW MANAGEMENT

Some of the best practices in cash flow management are highlighted as below:

(a) Calculate Gross Profit Margin

Gross profit margin is your gross profits shown as a percent of revenue. You need to really understand gross profit margins so you will know when to increase prices on which products and services. Increasing your prices, at the right time on the right things, is the best ways to impact cash flow, and as a result, your gross profit margin.

Looking at gross margin percentage is the best way to track the profitability of a customer or job.

Tracking gross margin every month and comparing it to your target gross margin, gives a business owner leading indicators of cash flow problems. A change in gross margins can provide insight into issues with a job, client or the company. This kind of actionable intelligence will help with pricing decisions.

(b) Implement Job Costing

The best way to monitor gross profit $ (or any other currency used in the economy) and % is to implement some form of job costing.

A well-designed job costing system tracks the true costs to deliver a service or product so you can charge prices that help achieve target gross profit margins and improve cash flow.

If you make money on your people’s time, you need to implement a simple time tracking system to see if you’re allocating the right fees for the time spent on the job.

The biggest benefit of true job costing works is knowing that nothing slipped through the cracks and you're getting paid for all the value that you delivered.

(c) Understand Fully Loaded

Labor Costs

Understanding your true fully loaded labor cost will help make sure your proposals and price quotes achieve your target gross profit percentage.

This will help you get your pricing right and solve most of your cash flow problems.

You can cover all your costs and bill for all your value if you know, and can explain, what it really takes to deliver on each job. Having visibility into real costs allows you to include details of all your value and time spent in your proposals, which will help you sell a higher dollar amount on every job. (Visibility into time leakage helps eliminate waste)

Compare your gross profit percentage on every job against what you expected it would be and your industry averages. That will help you increase the accuracy and value pricing in future proposals.

Cost of Goods Sold (COGS) is an important number to help with your pricing because it’s used to calculate gross profit on a job. Make sure you know what your fully loaded hourly labor cost (with full true fringe benefits) is costing you. Do you understand how COGS relates to your organization's gross profits?

(d) Measure DSO

You Cannot Manage What You Cannot Measure What management monitors gets done. You can’t manage what you don’t measure. To measure your cash flow, you need to keep track of Days Sales Outstanding (DSO). You want to reduce your DSO to the smallest number possible. Why? Because every day you’re doing work that you haven’t been paid for. Unless you’re in the business of lending people money-you should reduce your DSO.

Every day that you're doing work that your client hasn't paid for upfront, you're essentially giving that client a loan. DSO measures the number of days it takes to collect a dollar of sales. It’s the average age of your accounts receivable-if your average is trending higher, then your business is more likely to struggle with cash flow. Knowing your DSO can also help determine whether or not you need to improve your current processes and policies or outsource collections.

The easiest way to reduce DSO is with timely billing through lightning fast invoicing, and fast payment incentives like keeping a credit card on file or shortening net terms for payments.

(e) Institute a 2 Week Delay in Payroll Start

Implement a two-week waiting period between the time someone finishes work and the time you pay them. After you set it up, it only affects new employees.

Setting up a delay in a payroll start serves two purposes:

1. It allows you enough time to invoice and possibly get paid by your client.

2. It gives you more time to process that payroll so it reduces the chance of errors.

For most service businesses, payroll is their biggest expense, accounting for roughly 70% or more of expenses. The best practice of managing cash flow of paying expenses is related to managing the timing of your payroll. The goal is to pay payroll after you’ve been paid by your client-or at least to reduce the time period between when you pay payroll and when you get paid by your client.

Implement a two-week waiting period between the time someone finishes work and the time you pay them.

(f) Automate Invoicing

One of the most important ways to improve cash flow is to map out the steps involved in getting a bill out the door.

Ask yourself questions like:

1. How many people are involved in creating an invoice?

2. Once you’ve completed a job, how long does it take to get the invoice into the clients’ hands?

Studying and streamlining the billing process will speed up the time to get an invoice into a client’s hand and reduce the cost of invoicing customers, both of which will improve your cash flow.

(g) Get Paid in Advance (If Possible)

When you start a new job knowing you won’t have a negative cash balance, you’re already on the right track. Getting paid in advance is the way to avoid situations where you need to chase clients that delay payments. Is it likely? It depends on how much trust you have with your client. In some cases, it may help to offer a small discount for advance payment as an incentive. Advanced payment gives you peace of mind by reducing risk of nonpayment. It allows you to reinvest the money and lets you do better budgeting. Ask for the largest amount you can get before you start work when they are in love with the idea of working with you. 50% is standard in many industries.

(h) Get a Deposit Upfront Before Work Begins

Get 50% upfront on every job and you will immediately change from a mindset of scarcity to one of abundance. Why? Because, since many jobs target 50% gross profit percentage, you will have covered all your costs at the start of the job.

If you manage the job right, you don’t have to worry about getting the next check to make payroll. There’s a big difference between 33% and 50% - Shoot for 50% if you can.

Get 50% upfront on every job and you will immediately change from a mindset of scarcity to one of abundance.

Deposits are intended to cover your costs, so you minimize your risks.

Remember: A deposit upfront ensures trust and relieves some of the risk of non-payment. You need to establish trust with the prospect to get money up front.

(i) Set up a Retainer

Retainer billing is a no-brainer. It’s good for both you and your clients. A retainer program makes it easier for clients to budget and smooth out cash flow.

Look at how much your biggest clients pay you on an annual basis. Divide that by 12 to come up with a monthly amount. Give them a proposal that lists the services they use over the course of a year. Include a scope document that defines what they get for that monthly fee and what’s out of scope and covered by a pre-approved work order.

This enables both parties to map cash inflows and outflows more easily. It helps you reduce your billing and collections costs, and it helps them reduce their accounting costs.

(j) Bill Immediately at Project Completion

If you finish a job on the fifth of the month but you don’t send out the invoice until the end of the month, and the client pays you 30 days later, you’re not going to get paid for 55 days. You probably have payroll at least three - four times during those 55 days.

You should invoice the client as soon as possible, weekly, at milestones, or as soon as the job is done. As soon as you finish a job, bill the client the same or next day if you want to get your money faster. If you have service people working in the field, get them an account so you can get paid before they leave the job site.

If you focus on getting your money faster, you’ll be well on your way to improving your cash flow. You should invoice the client as soon as possible, weekly, at milestones, or as soon as the job is done.

(k) Get Cash before Payroll

In the ideal world, you get cash from your customers on a project before having to pay payroll related to that project. That’s the holy grail of cash management-but it's not always possible in every industry and business model.

But you can shrink the time between when you get paid and when you have to pay payroll. This has a material impact on cash flow. The bigger and more successful you are, the more important that becomes. Why? Bigger companies need more cash to survive and the cash flow risks are greater. Whether you're a $500,000 company or a $5 million company or whichever the size might be, you have to make every payroll. A big reason why so many small businesses fail is because they spend their time chasing cash just so they can make the next payroll.

(l) Assign a Collections Owner

Don’t assign collections to a receptionist or office manager unless you’ve made it clear where it fits on the priority list and given them sufficient time to do it right. A receptionist can’t make collection calls if he or she also has to answer the phone.

This is a cash flow mistake a lot of businesses make simply because the person making the call doesn’t want to do it, hasn’t been trained in conducting effective collections calls; and isn't given sufficient time for this time consuming, stressful task. As a result, collections becomes a low-priority job. One option is to have the sales person be accountable for the collection process. If they get paid when the company gets paid, you’ll have someone incented to make sure you get your money.

A bad collections process will lead to unnecessary cash flow problems. Collections are often the last thing anyone wants to do, so oftentimes it rarely gets done well.

(m) Call Clients 5 Days before Bills are due

Most people wait until the invoice is 30 days past due to make the first call. That’s a big mistake. Your first call to a client should occur between three and five days before the invoice is due.

Frame it as a client service call to check on the client's level of satisfaction while also checking to ensure that the invoice was received and understood. And get a commitment as to when you can expect payment.

Be ready to respond to any client service issues. People will tell you what’s wrong with your service delivery model when you are trying to separate them from their cash.

(n) Prepare for Collections Calls

One quick way to improve collection performance is to train your staff to anticipate what the client might say when you ask, “When can we count on you to pay your bill?”

They need to always be ready for possible responses when you call a client who has a past due bill. Here are the common excuses and some answers that can help your collections:

If you can be ready with a response and anticipate any objections your clients may have, then you will improve your cash flow.

(o) Fire Low Margin Clients

Fire Low Margin Clients & Re-assign Staff to Higher Margin Projects

If you keep low-margin clients out of fear of losing cash flow or not being able to replace them with a higher margin client, you will stunt your business growth.

Do not be afraid to fire low-margin clients-after all, Low Gross is Grief (LGIG). LGIG means your lowest margin clients usually give you the highest amount of grief and eat up your staff’s valuable time. Eliminate those clients, and you’ll have a more profitable business and a happier team.

Evaluate which clients should be fired, and increase your revenue and your profits by replacing the lowest margin clients with higher margin clients before you hire any new staff.

(p) Sort A/R Aging by Amount not alphabetically

When you start the collection process, the first step is to create the aged A/R report. Sort the aged A/R report by largest amount, not by account name.

Most accounting systems default their accounts receivable aging to an alphabetical listing. This puts the A’s up front. Instead, sort your A/R aging reports by the highest amount owed.

Focus on the largest balances, and you'll get the greatest returns.

(q) Follow the 3 F's of Collections: Be Firm, Focused, & Friendly

Be Firm

If you get a pay date commitment, you can call the day before and say, “We have you in our system for payment tomorrow. Can we count on that payment?”

Be Focused

If the client gives you any feedback about your service, make sure you’re listening carefully and address any concerns immediately. These actions will show that you’re serious about high quality service-and getting paid.

Be Friendly

Always be friendly and provide the highest-level customer service you can to help them through the process and make it minimally stressful for them as possible. This will help the customer feel comfortable and eager to help resolve the late payment issue.

(r) Check Background, Credit Rating and Credit References

If you’re not getting paid upfront for your services, you’re giving your clients a loan. You didn’t get into business to be a loan officer, but that’s the reality of providing services “on account.” Before issuing a loan do what a bank does. Don’t give out credit until you see if they are credit worthy

(s) Establish a Written Credit Policy

In addition to checking credit worthiness, make sure you have a written credit policy. This credit policy should be included in the terms and conditions of your proposal or contract and referenced in your invoices. Make sure everyone, including the client, knows the details regarding the rules of your company’s billing and collection practices, before you start doing any work.

At the very minimum, the written policy should include:

Payment Terms

- When is the balance due?

- Who is the person paying the bills?

- When does the client/company pay invoices?

Late Fees

- What are they, and when are they going to be charged?

- We recommend between 1.5% (18% annually) and 1.8% (21.6% annually) per month once a payment is late.

- “Don’t let your clients’ cash flow problems become your cash flow problems.

Legal Fees

- In the fine print, spell out who will pay attorney fees if you have to go to court to collect your payment.

(t) Audit Expenses

If you can cut expenses by 10%, the effect on your profits will be exponential. Plus, it’s usually easier than ramping up sales. Where can you decrease expenses to increase profitability without damaging productivity? Look at all your expenses, line by line, to understand if you truly need to incur each expense.

Analyze how it contributes to new sales or retention of current clients. Look at your overhead; you do not want this number to grow unless it has to.

(u) Implement Pay Slow Rule

Make sure the person paying the bills doesn’t have a “clean desk” rule. You should pay the bills when they are due and no sooner. If there are any discounts available, make sure you take all discounts that anyone offers you. Stretching payables to their due date can improve cash flow by simple timing, especially in the long run.

(v) Experiment with Your Pricing Model

The number one reason businesses fail, is they’re not pricing their jobs or services right. How well you price your products or services, and the margin that pricing produces, is key to maximizing cash flow.

You should put more thought into optimizing your pricing model, as this will have the biggest impact on cash flow. Consider the pricing model that fits best for your business: Value-Based, Fixed Fee, Time & Material, or Milestone Driven.

You have to have your prices cover your direct costs. They have to recapture your overhead, and give you a profit. So how do you optimize your pricing model to increase your company's profitability? You turn to your management reports and look at the data.

Management reports help you figure out if you are pricing your jobs right, and also to help you to really understand who your most profitable clients are, and what makes them profitable.

Consider the pricing model that fits best for your business:

(A) Value-Based Pricing Model

Value-based pricing is the method of setting a price by which a company calculates and tries to earn the differentiated worth of its product for a particular customer segment when compared to its competitor.

To understand how value-based pricing works, let’s take the example of Brand A that is about to launch a new LED television. It wants to figure out the price for its new 65-inch LED TV, the biggest screen size in the marketplace at the time. The company’s closest competitor, Brand B, recently introduced a 60-inch TV for $799. Both TVs have other features that are similar-both have built-in WiFi, the same level of definition, same number of HDMI inputs, same refresh rate, and so on.

Now let’s apply value-based pricing by considering each part of the definition carefully:

(1) Focus on a single segment. The first thing to know about value-based pricing is that it always references one specific segment. (For B2B products, it can be a single customer). Brand A’s focus is only on big-screen TV buyers, not all TV buyers. Marketers can’t use value-based pricing unless they have a specific segment. If they have multiple segments, they must determine a suitable value-based price for each one.

(2) Compare with next best alternative. This pricing method only works when the target segment has a specific competitor’s product they can buy instead. Value-based pricers always ask the question: “What would this segment buy if my product wasn’t available?” This “next best alternative” for the target is the essential point of comparison for calculating the value-based price. For products that are truly new, without peers, the value-based pricing methodology won’t work well.

(3) Understand differentiated worth. The next task is to figure out which product features are unique, that is, differentiated, from the competitor’s offering. In our case, the only differentiated feature of Brand A is its larger screen size.

(4) Place a dollar (or any other currency) amount on the differentiation. The last, and arguably the most difficult, step in calculating value-based price is to estimate the dollar value of the differentiated features. For us, this boils down to: “How much will big-screen TV shoppers pay for an extra 5 inches of screen size?” and then add that amount (let’s say it is $150) to $799, Brand B’s price. The value-based price of Brand A’s TV is $949. To accomplish this step, marketers typically use research methods like conjoint analysis or qualitative customer interviewing.

One final point about value-based pricing is this. Just because the differentiated worth is $150 doesn’t mean the company will get it all. In many situations (buying or renting a house for example), there will be a negotiation process, and the marketer may have to share the differentiated worth with the customer.

Dispelling Key Misconceptions about Value-Based Pricing

Value-based pricing is used in virtually every industry, to price everything from TVs and drugs, to oil rigs and airplanes. Despite its popularity, marketers have significant misconceptions about the approach. Here are three of the most common ones.

Misconception 1: Value-based pricing requires the company to evaluate consumers’ willingness-to- pay for each and every product feature. Some marketers wrongly believe that when a company uses value-based pricing, it has to assess how much the customer values every single product feature, assign a dollar amount to each one, and then add them all up to calculate the product’s final price. Even the simplest products have dozens of features. Imagine the difficulty of pulling this off for an oil rig or even a TV. This misconception turns many marketers off at the outset.

In reality, feature common with the next best alternative is captured by its price. In our TV example, the fact that both TVs have 3 HDMI inputs, built-in Wifi, and 4K Ultra HD is included in Brand B’s $799. We do not have to calculate each feature’s value separately. The only thing Brand A has to do is find the feature differences and assess customers’ valuation of these differentiated features. This is a lot easier to do.

Misconception 2: Even if competitors are not smart with pricing, using value-based pricing will lead to success. This is likely the most dangerous misperception about value-based pricing because it can create false, high expectations. Many marketers think that value-based pricing is a panacea. If they use it, they will make lots of money under any circumstances. Not true! The success of value- based pricing depends on how smartly competitors have priced their products. If they have set untenably low prices, value-based pricing can’t save you.

Just imagine what would happen if Brand B foolishly chose to sell its TV at $399 instead of $799. Brand A would still be only able to charge the $150 extra for its larger screen size, not any more. It would end up with a low price, and perhaps even lose money because of Brand B. Competitors have to practice “intelligent pricing” if value-based pricing is to work successfully.

Misconception 3:

You may also like...

-

Side Hustles that actually work Business by Godfrey OnyangoSide Hustles that actually work

Reads:

0Pages:

82Published:

Apr 2026*Side Hustles That Actually Work* is a practical guide to building real, sustainable income streams outside a full-time job. It cuts through generic advice by...

Formats: PDF

-

Your Next 60 Seconds: Mastering Quick and Effective Decision Making for Positive Results Business by JD KingYour Next 60 Seconds: Mastering Quick and Effective Decision Making for Positive Results

Reads:

91Pages:

147Published:

Oct 2025“Your Next 60 Seconds” provides us with a comprehensive guide to enhancing our decision-making skills in a fast-paced world. The book emphasizes the importanc...

Formats: PDF, Epub, Kindle, TXT

-

Bussiness is Money Business by Kazi Rejwan IslamBussiness is Money

Reads:

104Pages:

46Published:

Sep 2025Money Psychology in Business: Unlocking the Mind Behind Financial Decisions. Do smart people make poor money choices in business? How do emotions like fear, g...

Formats: PDF, Epub, Kindle, TXT

-

Writing, Branding, Content Creation Business by Caleb OlayiwolaWriting, Branding, Content Creation

Reads:

76Pages:

29Published:

Aug 2025"Writing, Branding, Content Creation" is a book written by Caleb Olayiwola. Available in PDF, the ebook talked about what writing is in details and expanded o...

Formats: PDF, Epub, Kindle, TXT